The US Dollar saw a marginal rise on Thursday as investors reevaluated their predictions for the extent of rate cuts by the Federal Reserve in the coming year. This cautious sentiment prevailed following a robust risk rally in the previous month, as reported by Reuters.

In Asian trading, the greenback reached a more than two-week high against the yen, benefitting from the return of full-scale trading with Japan back from an extended New Year break. The dollar peaked at 143.90 against the yen, marking a noteworthy increase of over 0.9% in the previous session – its most substantial gain since October. The current exchange stands at 143.75.

Conversely, the Australian dollar, often considered a gauge of risk appetite, faced challenges in rebounding from Wednesday’s two-week low of $0.6703 and last traded at $0.6744. The New Zealand dollar, also sensitive to risk, changed hands at $0.6266, hovering near a two-week low of $0.6221 from the previous session.

COOLING ECONOMY

The release of minutes from the Fed’s December policy meeting on Wednesday indicated officials’ confidence in gaining control over inflation. However, there was a lack of clear signals regarding the timing of potential rate cuts, as policymakers still deemed it necessary to keep rates restrictive for some time.

Christopher Wong, a currency strategist at OCBC, noted, “The messaging that rates will stay elevated raises a second look at the aggressive cut expectations markets are pricing.” He attributed the U.S. dollar’s rebound to factors such as global growth concerns, risk-off sentiment in U.S. equities, and the partial unwinding of aggressive bets on Fed cuts.

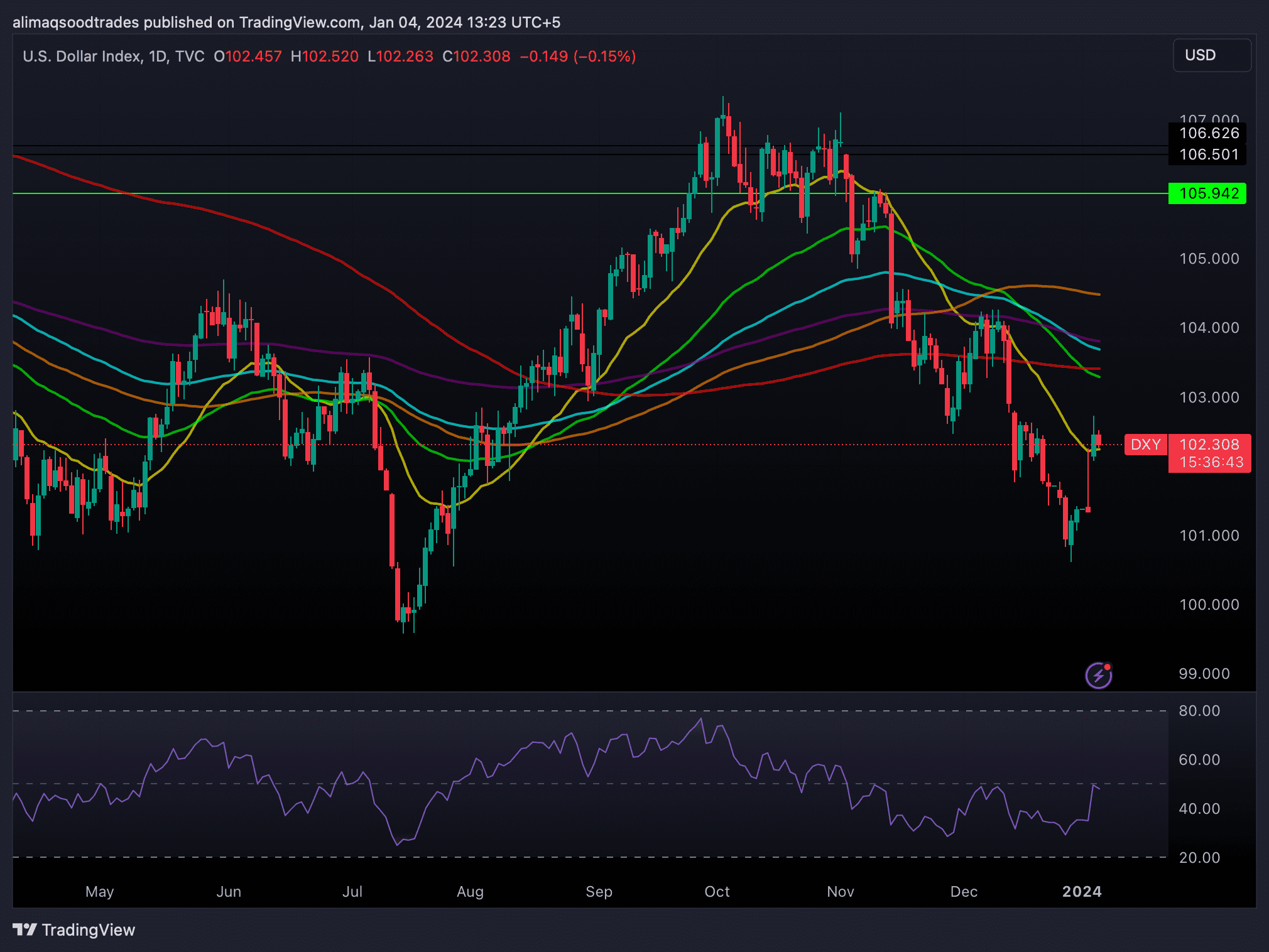

Against a basket of currencies, the greenback rose by 0.03% to 102.43, approaching the three-week peak of 102.73 reached in the previous session. The euro experienced losses but edged up by 0.09% to $1.0931, while sterling remained close to its recent three-week low at $1.2667.

Recent data exhibits a further contraction in U.S. manufacturing in December, albeit at a slower pace. Additionally, U.S. job openings fell for the third consecutive month in November, indicating easing conditions in the labor market.

As the U.S. economy shows signs of cooling, expectations of Fed rate cuts persist. However, traders remain divided on the timing and scale of potential easing. Market pricing now indicates a roughly 72% chance of the Fed initiating rate cuts in March, down from 87% a week ago, according to the CME FedWatch tool.

The eagerly awaited U.S. nonfarm payrolls report, which is expected to shed more light on the Fed’s potential room for rate adjustments, is what investors are waiting for this Friday.